28 November 2017

Christmas will be here before we know it, with smarter business owners already planning their end-of-year festivities. Celebrating the season can be team-building or just a bit of fun, but the well-prepared business owner will also know that a little tax planning can help make sure there’s no unforeseen tax problems.

The three benefits typically provided include:

- Christmas parties for employees (and perhaps their family members, and even clients)

- gifts to employees, their family members and clients, and

- cash bonuses.

The Christmas party

There is no separate FBT category that relates to Christmas parties. While such social functions may result in FBT, income tax and GST outcomes, these are covered under the existing relevant legislation. The provision of “entertainment” at Christmas therefore mirrors the tax treatment such benefits will receive at other times of the year.

The ATO says that “meal entertainment”, and therefore an FBT liability, arises when food or drink is provided in a way that has the character of entertainment. In fact, the ATO holds that in most cases the mere provision of food or drink satisfies the “entertainment” test, but adds that there is a narrow category of cases where the mere provision of food or drink does not amount to entertainment.

For example, it considers that the provision of morning and afternoon tea to employees (and associates of employees) on a working day, either on the employer’s premises or at a worksite of the employer, is not entertainment. The provision of light meals (finger food, etc), for example in the context of providing a working lunch, is also not considered to be entertainment. Note however that providing any alcohol typically brings “entertainment” into the picture.

The implications of certain benefits provided at the year-end Christmas function for an employer may vary depending on:

- whether the function is provided at the employer’s premises or provided externally

- the cost of the function per attendee, and

- the basis that the employer is using in working out the taxable value of such benefits.

FBT implications

With a Christmas party, FBT applies to an employer when they provide a benefit to an employee or their associate (for example, family members). Food, drink, entertainment and gifts provided at a Christmas party to employees and their associates may constitute either:

- an expense payment fringe benefit (eg. reimbursing an employee for expenses incurred or paying an expense on their behalf)

- a property fringe benefit (eg. provision of property such as meals or gifts by the employer), and

- a residual fringe benefit (eg. the provision of any right, privilege, service or facility such as the right to use a venue).

These benefits are generally valued for FBT purposes at their face value – typically referred to as an “actual basis” of valuation. However, an employer may elect to apply special valuation rules by using either the 50/50 split method or 12-week register method. Ask us about these two valuation methods and if they are suitable for your business. If the employer does not make an election, the taxable value is determined according to actual expenditure.

However “meal entertainment” fringe benefits provided at a Christmas function can be exempt from FBT if it is:

- a “minor benefit” (more below)

- an exempt property benefit (see below) is provided at the employer’s premises on a work day.

Minor benefits

Broadly, a minor benefit is one where it:

- has a notional taxable value of less than $300 (inclusive of GST)

- is provided on an “infrequent” or “irregular” basis

- is not a reward for services, and

- satisfies other relevant conditions (ask us for details).

Note that other benefits (such as gifts) provided at a Christmas party may be considered as separate minor benefits in addition to meals provided (referred to as an “associated benefit”). In such cases, the $300 threshold generally applies separately to each benefit provided.

Exempt property benefit

A Christmas party held at the employer’s business premises on a working day where food and drink, including alcohol, is provided is generally deemed to be an exempt property benefit, and is therefore usually FBT-free. This is no different to the occasional Friday drinks at work.

Tax law exempts such property benefits where:

- the benefit is provided to a current employee in respect of his or her employment, and

- it is provided to, and consumed by, the employee on a working day and on the business premises of the employer.

This exemption applies only to employees. Where members of the employee’s family (“associates”) also attend a function (such as the Christmas party), the cost attributable to each associate is subject to FBT unless it is a minor benefit. If clients are invited to the function, the cost of providing the entertainment to these attendees is excluded from the FBT regime as this not a “fringe benefit” to staff (and may qualify as a tax deduction — see below under “Gifts to clients”).

External Christmas functions

The costs associated with Christmas parties held off business premises (such as food, drink and transport to a restaurant) will give rise to FBT unless these costs are under the minor benefit threshold. Again, FBT will not apply to the extent that the benefit is provided to a client.

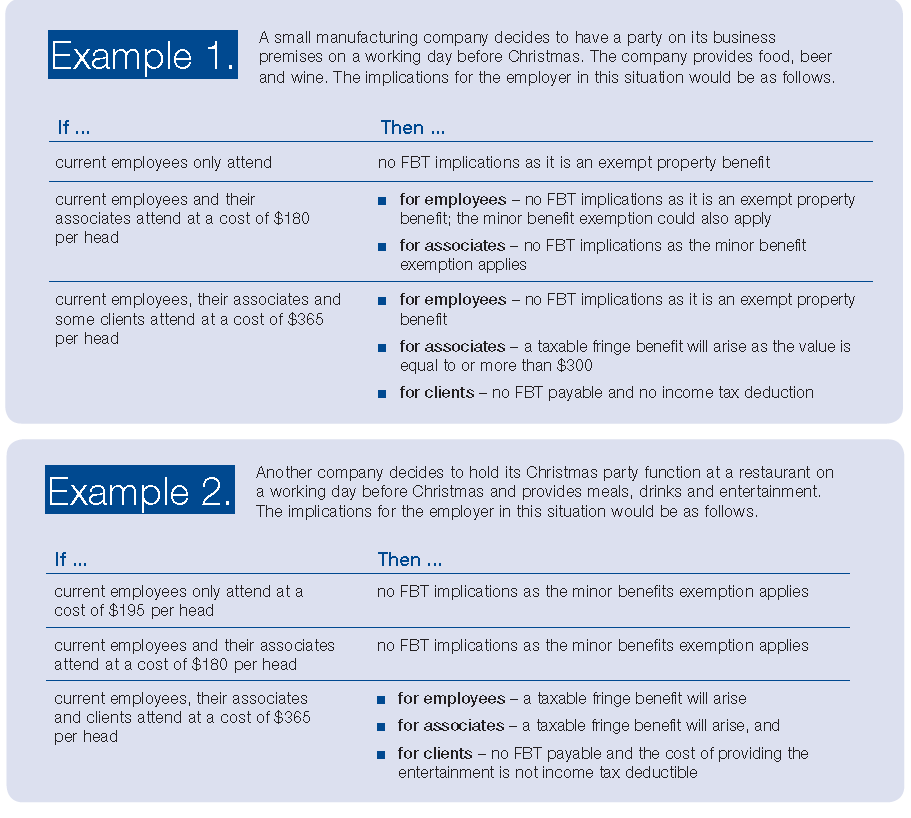

The following examples supplied by the ATO illustrate the difference in FBT and income tax treatment where a function is held on-premises compared to one being held offsite:

Transport considerations

It may be the case that to get to the Christmas function, an employer will provide their staff with taxi travel or some other form of transport. Taxi travel provided to an employee will generally attract FBT unless the travel is for a trip that either starts or ends at the employee’s place of work.

For taxi travel to or from a Christmas function, employers should be mindful that:

- where the employer pays for an employee’s taxi travel home from the Christmas party and the party is held on the business premises, no FBT will apply.

- where the party is held off premises and the employer pays for a taxi to the venue and then also pays for the employee to take a taxi home, only the first trip will be FBT exempt. The second trip may be exempt under the minor benefits exemption if the employer has adopted to value its meal entertainment on an actual basis.

- the exemption does not apply to taxi travel provided to “associates” of employees (for example family members).

If other forms of transportation are provided to or from the venue, such as bus travel, then such costs will form part of the total meal entertainment expenditure and be subject to FBT. A minor benefit exemption for this benefit may be available if the threshold is not breached.

Gifts

Gifts provided to employees or their associates will typically constitute a property fringe benefit and therefore are subject to FBT unless the minor benefit exemption applies. Gifts, and indeed all benefits associated with the Christmas function, should be considered separately to the Christmas party in light of the minor benefits exemption.

For example, the cost of gifts such as bottles of wine and hampers given at the function should be looked at separately to determine if the minor benefits exemption applies to these benefits. Gifts provided to clients are outside of the FBT rules (but may be deductible, see below – also note that deductibility may still apply even if the gift is a “minor benefit”).

The income tax deductibility and entitlement to input tax credits (ITC) for the cost of the gifts depends on whether they are considered to be “entertainment”. For example, an unopened bottle of spirits is deemed to be a property benefit (the entertainment starts after the cap is unscrewed). Again, in most cases the entitlement to an ITC for expenses incurred for the employer mirrors the income tax implications – so an ITC is only available to the extent that the expense incurred is deductible.

Examples of “entertainment”:

- glasses of champagne

- hot meals

- theatre tickets

- holiday accommodation

- hired entertainers

- hired sporting equipment.

Examples – not “entertainment”:

- Bottled spirits

- groceries

- games

- TV sets, DVD players

- computers

- crockery

- swimming pools

- gardening equipment

Gifts to clients

Regarding a business providing a gift a client, even a former client, the ATO confirms that such outgoings are generally deductible as they are being made for the purposes of producing future assessable income. However, the outgoing is not deductible where it is of a capital nature, relates to the gaining of exempt or non-assessable non-exempt income, or some other provision of the income tax law prevents it from being deductible.

To explain this quirk, the ATO provides the following examples:

Example 1. Julia is carrying on a renovation business. She gifts a bottle of champagne to a client who had a renovation completed within the preceding 12 months.

Julia expects the gift will either generate future business from the client or make them more inclined to refer others to her business. Although Julia got on well with her client, the gift was not made for personal reasons and is not of a private or domestic character.

The outgoing she incurred for the champagne is not of a capital nature. Julia is entitled to a deduction.

Example 2. David is carrying on a business of selling garden statues. David sells a statue to his brother for $200. Subsequently, David gifts a bottle of champagne to his brother worth $170. Apart from this transaction, he provides gifts only to clients who have spent over $2,500 over the last year.

The gift has been made for personal reasons, and is of a private or domestic character. David is not entitled to a deduction.

Cash bonuses

Some generous/successful employers, budget permitting, may choose to provide cash bonuses to staff in their end-of-calendar-year payroll. Bonuses in the form of cash are considered to be a business cost, and therefore deductible under the general deduction provisions.

However, being a benefit in the form of “coin” there is another side to this coin, which is that cash bonuses are assessable in the hands of employees as ordinary income, no differently to salary and wages.

As a cash bonus is salary and wages, it is therefore not a taxable supply for GST purposes – so for these type of benefits, GST issues do not arise. Also there are no FBT issues to consider. However employers should consider PAYG withholding, superannuation guarantee and payroll tax issues. We can help with these decisions.